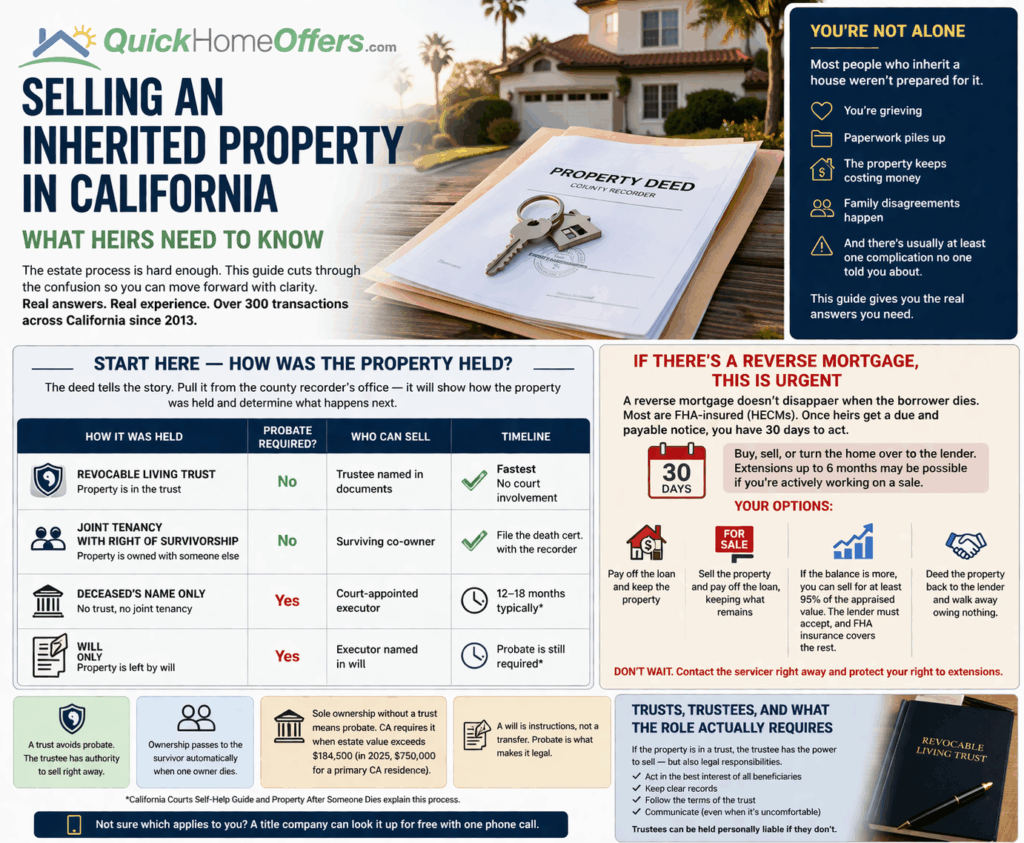

Most people who inherit a house in California weren’t prepared for it. The estate process often arrives when you’re still grieving. The paperwork piles up fast, and the property itself — possibly wrapped in family disagreements — keeps costing money while everyone figures out what to do next. And underneath all of it, there’s usually at least one complication nobody told you about: a reverse mortgage, unpaid taxes, a sibling who won’t cooperate, liens or title issues, or a building in far worse shape than anyone realized.

This guide is for heirs who need real answers, not a glossy overview of the selling process. It covers what actually gets in the way of selling inherited property in California and what to do about it. The experience behind it comes from Adam and Josh Justiniano at Quick Home Offers®— over 300 transactions across California since 2013. A significant number of them were inherited properties in exactly the situations described here.

Ok, here’s the part where we cover our bases. This guide is here to help you understand the general process of selling an inherited property in California — but it’s not legal advice. We’re real estate buyers, not lawyers, and we don’t play them on TV either. If you’ve got legal questions, those belong on a lawyer’s desk, not ours. Now, back to the good stuff.

Start Here — How Was the Property Held?

Before anything else can move forward, you need to know how the property was titled. This one question determines who has authority to sell, whether probate is required, and how long the whole process will take.

The easiest way to get this information is by pulling the deed from the county recorder’s office. The vesting language on that document will tell you exactly how the property was held, and everything else flows from that answer. You can also contact your attorney or call a local title company — most will pull the information for you at no cost.

| How It Was Held | Probate Required? | Who Can Sell | Timeline |

| Revocable Living Trust | No | Trustee named in documents | Fastest – No court involvement |

| Joint Tenancy | No | Surviving Co-Owner | File the death cert. with the recorder |

| Deceased’s Name Only – No Trust or Joint Tenancy | Yes | Court-appointed executor | 12-18 months typically |

| Will Only | Yes | Executor named in will | The will instructs the court — probate is still required |

Held in a revocable living trust: The trustee named in that document has immediate authority to sell without going through probate. This is the fastest path, and the one most California homeowners who did any estate planning will have set up.

Held in joint tenancy with right of survivorship: Title passes automatically to the surviving co-owner when one owner dies. Filing a certified copy of the death certificate with the county recorder is typically all that’s needed to clear the title.

Held solely in the deceased’s name — no trust, no joint tenancy: You’re looking at probate. California requires it when the total estate value exceeds $184,500. It’s the slowest and most expensive path, and it typically takes 12 to 18 months to complete. A 2025 change in this law raises the limit to $750,000 only for a decedent’s primary California residence. The California Courts Self-Help Guide explains how to determine whether your situation requires formal probate. Formal probate typically takes 12 to 18 months to complete.

Held by will only — the scenario that surprises most heirs: A properly executed will does not transfer ownership on its own. A will is a set of instructions to the probate court about who should receive the property. Even with a valid, witnessed, and notarized will in place, the estate must still go through probate before title can legally transfer. The will determines who inherits — probate is still the process that makes it happen. The California Courts overview of property after someone dies covers this clearly.

If you’re unsure which of these applies to your situation, a title company can usually tell you in a single phone call after looking up the property. It costs nothing to ask, and it tells you exactly what you’re working with before any decisions are made.

If There’s a Reverse Mortgage, This Is Urgent

A reverse mortgage doesn’t go away when the borrower dies. Most reverse mortgages today are Home Equity Conversion Mortgages — HECMs — insured by the Federal Housing Administration. According to the Consumer Financial Protection Bureau, once heirs receive a due and payable notice from the lender, they have 30 days to buy, sell, or turn the home over to the lender. There is the possibility of extensions up to six months for heirs actively working toward a sale. Note that other reverse mortgage products exist, such as proprietary jumbo reverse mortgages, which may have different terms. Talk with the loan servicer to be sure.

Your options as an heir:

- Pay off the loan balance and keep the property

- Sell the property and use the proceeds to pay off the loan — keeping whatever remains

- If the balance exceeds the home’s value, HUD’s guidance allows you to sell for at least 95% of the current appraised value, and the lender must accept that as full satisfaction — FHA insurance covers the rest

- Deed the property back to the lender and walk away owing nothing

We’ve purchased California homes with active reverse mortgages in Sacramento, Palm Springs, and elsewhere across the state. In practice, a reverse mortgage sale works like any other transaction once everyone understands the timeline — the servicer gets paid at closing, escrow handles the mechanics.

The worst thing you can do when a reverse mortgage is involved is nothing. Contact the servicer immediately, document that you’re actively working toward resolution, and protect your right to those extensions from day one.

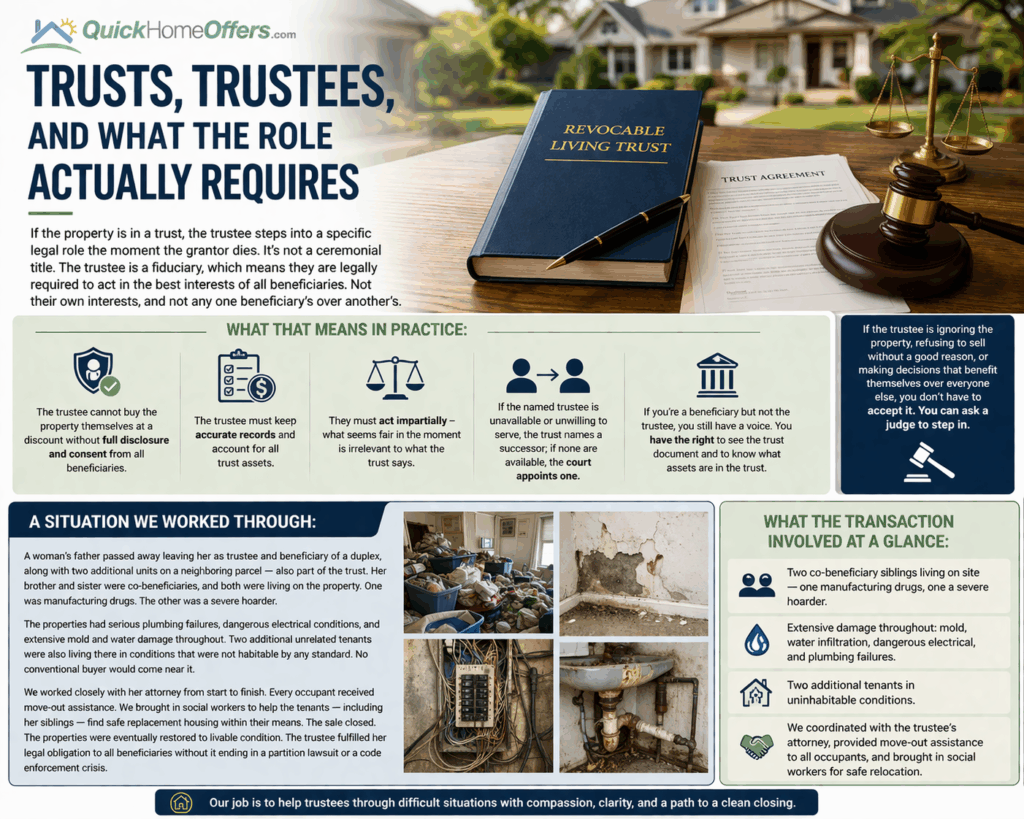

Trusts, Trustees, and What the Role Actually Requires

If the property is in a trust, the trustee steps into a specific legal role the moment the grantor dies. It’s not a ceremonial title. The trustee is a fiduciary, which means they are legally required to act in the best interests of all beneficiaries. Not their own interests, and not any one beneficiary’s over another’s.

What that means in practice:

- The trustee cannot buy the property themselves at a discount without full disclosure and consent from all beneficiaries.

- Trustee must keep accurate records and account for all trust assets.

- They must act impartially – what seems fair in the moment is irrelevant to what the trust says.

- If the named trustee is unavailable or unwilling to serve, the trust names a successor; if none are available, the court appoints one.

If you’re a beneficiary but not the trustee, you still have a voice. You have the right to see the trust document and to know what assets are in the trust. If the trustee is ignoring the property, refusing to sell without a good reason, or making decisions that benefit themselves over everyone else, you don’t have to accept it. You can ask a judge to step in.

A situation we worked through:

A woman’s father passed away leaving her as trustee and beneficiary of a duplex, along with two additional units on a neighboring parcel — also part of the trust. Her brother and sister were co-beneficiaries, and both were living on the property. One was manufacturing drugs. The other was a severe hoarder.

The properties had serious plumbing failures, dangerous electrical conditions, and extensive mold and water damage throughout. Two additional unrelated tenants were also living there in conditions that were not habitable by any standard. No conventional buyer would come near it.

We worked closely with her attorney from start to finish. Every occupant received move-out assistance. We brought in social workers to help the tenants — including her siblings — find safe replacement housing within their means. The sale closed. The properties were eventually restored to livable condition. The trustee fulfilled her legal obligation to all beneficiaries without it ending in a partition lawsuit or a code enforcement crisis.

What the transaction involved at a glance:

- Two co-beneficiary siblings living on site — one manufacturing drugs, one a severe hoarder

- Extensive damage throughout: mold, water infiltration, dangerous electrical, and plumbing failures

- Two additional tenants in uninhabitable conditions.

- We coordinated with the trustee’s attorney, provided move-out assistance to all occupants, and brought in social workers for safe relocation

What Happens to the Debts on an Inherited Property?

The short answer: secured debts follow the property; unsecured debts generally don’t. Anything recorded against the property as a lien — unpaid property taxes, mortgage balances, HOA liens, mechanics liens, recorded judgment liens — stays with the property when ownership transfers. These must be resolved at closing, but in most cases, they’re paid from the sale proceeds. You typically don’t need to come out of pocket before the transaction funds.

Credit card balances, medical bills, and personal loans are a different story. Those are claims against the estate, not the property itself. The heir who receives the house does not personally inherit that debt.

We’ve closed on California properties carrying more than a decade of delinquent property taxes across multiple Los Angeles County parcels. In every case, those balances were resolved through escrow — the sellers walked away with their net proceeds without funding anything upfront. On a separate transaction, a consumer debt judgment had been recorded against the property before the owner passed. We worked with the seller’s attorney to negotiate that balance down before closing, which allowed the sale to proceed cleanly.

Before anything else, ask a title company to pull a preliminary title report. It shows every recorded lien, takes a few days, and most title companies will do it at no cost when there’s a realistic chance of a transaction. It removes all the guesswork about what you’re actually dealing with.

What a Vacant Inherited Property Actually Costs Every Month

Every month, an inherited property sits empty, and the costs compound. These are real, recurring expenses that stack up quietly in the background while probate moves slowly or heirs work through disagreements.

| Monthly Cost | Estimated Range |

|---|---|

| Property taxes | $400 – $800 |

| Vacant property insurance | $150 – $400 |

| Utilities | $50 – $200 |

| Basic maintenance | $100 – $300 |

| Total monthly baseline | $750 – $1,700 |

Over a 12-month probate timeline, that’s $9,000 to $20,000 in carrying costs before you account for emergency repairs, code violations, or deferred maintenance that worsens while the property sits.

Beyond the money, a vacant property creates liability that falls directly on the trustee or executor:

- Standard homeowner’s insurance policies typically exclude coverage after 30 to 60 days of vacancy — if a pipe bursts or a fire starts, the claim may be denied.

- Code violations accumulate from overgrown landscaping, pest infestation, or structural deterioration — fines become liens

- Unauthorized occupants, squatters, or tenants who are not paying are harder to remove the longer they’ve been there — a formal unlawful detainer action in California typically runs several thousand dollars and can take months or longer to complete.

- Slip-and-fall or injury on an unmaintained property can generate a negligence claim against the estate

None of this is meant to rush a decision. It’s meant to ensure heirs make an informed one. A sale that nets $20,000 less than retail may still produce a better outcome when you factor in a year of carrying costs, a code violation or two, and a full probate timeline.

When Multiple Heirs Can’t Agree

More inherited property sales stall here than anywhere else. Clean title, no serious debt, a ready buyer — and the whole thing goes sideways because the heirs can’t get to a decision together.

The legal structure matters:

| Ownership Type | Who Can Sell | What Happens If Someone Refuses |

|---|---|---|

| Property in a trust | Trustee — no unanimous consent needed | Beneficiaries can petition the court if the trustee is acting improperly |

| Probate estate | Court-appointed executor | Beneficiaries can petition the court if the trustee is acting improperly |

| Tenants in common | All owners must agree | Beneficiaries can petition the court if trustee is acting improperly |

If the property was inherited as tenants in common (which is common when there’s no trust and multiple heirs are named), every owner must agree to a voluntary sale. A single heir can block the transaction indefinitely. When that happens, the other co-owners can file a partition action in a California court to compel a sale. It’s slow, expensive, and hard on family relationships. Most situations settle before it gets that far — but sometimes just raising the option is enough to break the stalemate.

The real obstacles in multi-heir situations are rarely legal. They’re logistical and emotional. Heirs live in different states or different countries. They have different financial pressures and different histories with the property. Getting everyone to the same place takes longer than the legal steps ever do.

Situations we’ve seen:

We’ve closed on properties where a key heir was in England — the entire process happened remotely through title and escrow. We’ve also worked through situations where an heir was living at the property and needed time to transition out before closing. Neither of those things made a sale impossible.

One thing that consistently moves things forward is putting a real offer on the table. Heirs who have been debating what a property is worth tend to focus when there’s an actual number in writing. It shifts the conversation from opinion to decision.

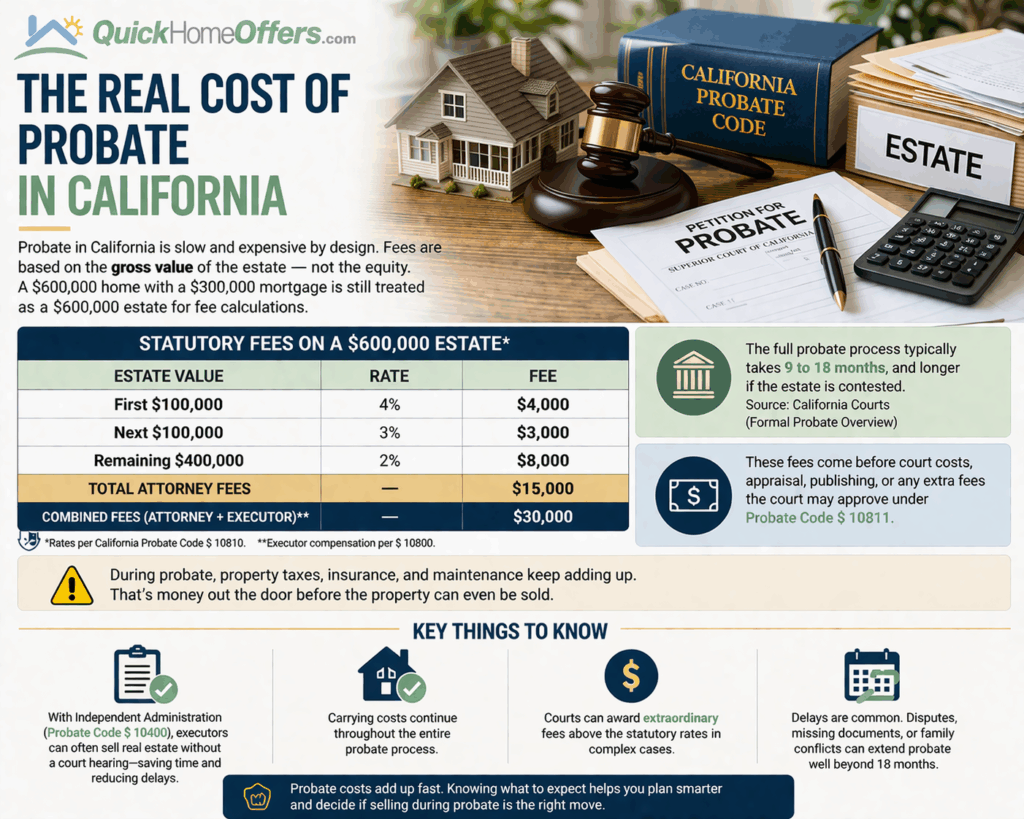

The Real Cost of Going Through Probate in California

Probate in California is slow and expensive by design. Fees are set by statute and calculated on the gross value of the estate — not the equity, not what’s left after the mortgage. A property worth $600,000 with a $300,000 mortgage is treated as a $600,000 estate for fee calculation purposes.

Attorney fees are set by California Probate Code § 10810, and the executor receives identical compensation under § 10800.

Statutory fee breakdown on a $600,000 estate:

| Estate Value | Rate | Fees |

| First $100,000 | 4% | $4,000 |

| Next $100,00 | 3% | $3,000 |

| Remaining $400,000 | 2% | $8,000 |

| Total Attorney’s Fees | — | $15,000 |

| Combined Statutory Fees | — | $30,000 |

That’s before court filing fees, newspaper publication costs, appraisal fees, or any extraordinary fees the court approves under Probate Code § 10811 for unusual circumstances. And it’s before a single month of carrying costs on the property itself.

The California Courts formal probate overview confirms the full process typically takes 9 to 18 months and can run longer for contested estates.

A few things worth knowing:

- An executor granted authority under the Independent Administration of Estates Act — Probate Code § 10400 can often sell property without a court confirmation hearing, which reduces the timeline meaningfully

- Property taxes, insurance, and maintenance continue to accrue throughout the entire probate period

- The court can award extraordinary fees above the statutory amounts — ask your attorney upfront whether your situation is likely to trigger them

What the IAEA can do for you — and what it can’t:

The Independent Administration of Estates Act — Probate Code §§ 10400–10592 is the single biggest timeline lever available in a California probate. It’s worth understanding in plain terms.

Under standard probate, the executor has to go back to court for approval on nearly every significant action — including selling real estate. That means scheduling hearings, waiting for court dates, and running the risk of losing a buyer while you wait. The IAEA changes that. When the court grants the executor IAEA authority — either because the will requests it or the executor petitions for it — most of those court appearances go away.

There are two levels. Full IAEA authority allows the executor to list and sell the property without a separate court confirmation hearing, essentially like a normal real estate transaction. The sale still requires a Notice of Proposed Action sent to all beneficiaries, giving them 15 days to object — but if no one objects, the sale can close without the court ever being involved in the property transaction itself. Limited IAEA authority is more restricted — the executor still needs a court order before selling real estate, which adds weeks or months to the process.

Full IAEA authority is generally necessary if there’s real property in the estate and speed matters. Most experienced probate attorneys request it at the very start by checking the appropriate box on the initial Petition for Probate. If it isn’t requested upfront, it can be added later — but that requires a separate hearing and additional delay.

Two important limits: IAEA authority is not automatic; it must be requested. And the decedent can prohibit it by saying so explicitly in their will. If you’re named executor and the estate includes real property, ask your attorney about IAEA authority on day one.

One significant tax advantage that heirs often overlook

According to the IRS, the basis of inherited property is generally the fair market value at the date of the decedent’s death. This stepped-up basis means that if you sell shortly after inheriting, you typically owe no capital gains tax on appreciation that occurred during the prior owner’s lifetime. If you hold the property and it appreciates further, you owe gains only on the increase above that stepped-up value. Talk to a CPA before making any decisions based on this — every situation is different.

When a Cash Sale Makes Sense

A cash buyer isn’t the right answer for every inherited property. If the house is in good condition, probate is closed, all heirs are aligned, and you have time, a traditional listing will likely net more money. We’ll tell you that directly.

But many inherited properties don’t fit that description. Here’s an honest side-by-side:

| Situation | Traditional Listing | Cash Sale |

|---|---|---|

| Property needs significant repairs | Limits buyer pool, reduces offers | No repairs needed — sold as-is |

| Active reverse mortgage deadline | Buyer financing may not close in time | Closes on your timeline |

| Delinquent taxes or liens | Must be resolved before listing | Resolved through escrow at closing |

| Multiple heirs, some uncooperative | Delays can kill deals | Offer in hand moves negotiations forward |

| Heir lives out of state or overseas | Complicated logistics | Fully remote close through title and escrow |

| Property in probate | Financed buyers won’t wait | Cash closes without financing contingencies |

| Property in habitable condition, no complications | List it — you’ll net more | Cash still available, but may not be necessary |

At Quick Home Offers, Adam and Josh Justiniano personally evaluate every property. No algorithms, no automated offers — one of us looks at what you have and gives you a straight number. We’ve been doing this since 2013 across more than 300 California transactions. We’ve handled delinquent taxes, recorded judgment liens, active reverse mortgage deadlines, uninhabitable properties, and multi-heir sales with heirs on two different continents.

If you want to know what we’d pay, call us at 805-870-5749 or submit the address below. No obligation.

Get An Offer Today, Sell In A Matter Of Days…

"*" indicates required fields

Frequently Asked Questions

Q: Do I have to go through probate to sell an inherited house in California?

A: Not always. If the property was held in a living trust, the trustee can sell without probate. If it was held in joint tenancy, title passes automatically to the surviving co-owner. Probate is required when the property was held solely in the deceased’s name and the total estate value exceeds $184,500 — though a 2025 law change allows a simplified transfer process for primary residences valued at $750,000 or less.

Q: How long does California probate take?

A: The California Courts put the typical range at 9 to 18 months, sometimes longer for contested estates. An executor with full Independent Administration of Estates Act authority can often sell the property without a court confirmation hearing, which shortens the timeline meaningfully. Without IAEA authority, every major transaction requires a separate court hearing and scheduling delay.

Q: What happens to a reverse mortgage when someone dies?

A: According to the Consumer Financial Protection Bureau, heirs receive a due and payable notice and have 30 days to act, with extensions available up to six months for heirs actively working toward a sale. For FHA-insured HECMs, HUD’s guidance protects heirs if the loan balance exceeds the home’s value: you may sell for at least 95% of the current appraised value, and the lender must accept that as full satisfaction.

Q: Will I owe capital gains tax when I sell an inherited house in California?

A: Generally, no, if you sell shortly after inheriting. According to the IRS, the basis of inherited property is stepped up to fair market value at the date of death. If you sell at or near that value, there is typically no taxable gain. If you hold the property and it appreciates before selling, you owe gains only on the increase above that stepped-up basis. Talk to a CPA — every situation is different.

Q: How does Proposition 19 affect an inherited property in California?

A: Proposition 19, effective February 2021, significantly changed the property tax rules for inherited homes. Unless the heir moves into the property as their primary residence within one year, the property is reassessed to the current market value, which can substantially increase annual property taxes. If you inherit a home your parents bought decades ago at a low assessed value, and you don’t plan to live there, expect a meaningful tax increase. The California State Board of Equalization has guidance on how the reassessment rules apply.

Q: Can one heir force a sale if the others won’t agree?

A: Yes. If the property is held as tenants in common and an heir refuses to sell, any co-owner can file a partition action in a California court to compel a sale. Partition actions are slow and expensive — most families reach an agreement before it reaches that point. If you’re in this situation, consulting a probate attorney about partition as an option — without necessarily filing — is often enough to move negotiations forward.

Q: What if the inherited property has liens or years of unpaid taxes?

A: Liens and delinquent property taxes follow the property and must be resolved at close of escrow. In most cases, they’re paid from the sale proceeds. You typically don’t need to come out of pocket before the transaction funds. We’ve closed on California properties with years of delinquent property taxes across multiple parcels. In every case, those balances were resolved through escrow.

Q: Can I sell an inherited house as-is without making repairs?

A: Yes. Cash buyers purchase properties in any condition. If you list on the MLS, property condition directly affects both your buyer pool and your final price — buyers requiring financing will often walk if inspections reveal significant issues. A direct cash sale removes that variable entirely.

Q: What if I live out of state or overseas?

A: Distance is not an obstacle. Signing, identity verification, and receiving proceeds can all be handled remotely through a title company and escrow. We’ve closed on California inherited properties with heirs in other states and other countries — the process works the same way regardless of where you are.

Q: What is IAEA authority, and should I ask for it?

A: The Independent Administration of Estates Act — California Probate Code § 10400 allows an executor to manage and sell estate property without going back to court for approval on every transaction. With full IAEA authority, a property can be listed and sold almost like a standard real estate transaction, without a court confirmation hearing. It must be specifically requested — typically when the initial Petition for Probate is filed. If the estate includes real property, ask your probate attorney about IAEA authority on day one.