If you can’t afford major repairs before selling your home in California, you are not stuck. You have several paths forward. You can sell the property as is to a cash buyer who will purchase it in its current condition—an as-is sale means you don’t make repairs or improvements, and the buyer accepts the home exactly as it stands.

You can list it on the open market and negotiate seller credits so the buyer handles repairs after closing. You can finance the repairs yourself through a home equity line of credit or personal loan. Or you can make specific low-cost improvements that improve buyer perception without touching the big-ticket items. Many homeowners face these challenges and must also weigh closing costs as part of their decision-making process.

The right path depends on how much work the home needs, how quickly you need to sell, and whether the property can qualify for traditional financing in its current condition. Closing costs are a key part of the net proceeds calculation when choosing which selling path is best.

This guide walks through every option, including which issues make a home unfinanceable, how to price a property that needs work, and your best options to net the most from your sale — based on our experience of over 300 transactions statewide since 2013.

What to Do If You Can’t Afford Home Repairs Before Selling — Quick Answer

If you cannot afford to make repairs before selling, an as is sale—where the seller will not make any repairs before closing and buyers purchase the property in its current condition—is typically the fastest path to closing. Cash buyers purchase the property as is, do not require inspections or lender approval, and can often close in as little as 7 to 10 days, making them especially attractive for sellers who need to sell fast. Keep in mind, buyers of as-is properties often account for the cost of repairs they will need to undertake after purchase.

You can also list the home as is on the open market with a real estate agent, though most traditional buyers will request an inspection and may ask for repair credits or concessions. This route is best for properties that need minor or cosmetic repairs.

Financing the repairs with a HELOC (home equity line of credit) is a good option if you have equity in the home and are doing a moderate

If the home has issues that prevent a buyer from obtaining a mortgage — such as a damaged roof, foundation problems, failing electrical or plumbing systems, missing flooring or windows, or code violations — if you sell “as-is,” your buyer pool is limited to cash buyers and real estate investors, regardless of which selling path you choose.

Is Your Home Financeable? Why This Matters Before You Decide

Before you evaluate your options, you need to answer one question: Can a buyer get a mortgage on your home in its current condition? If the answer is no, it changes everything about how you approach the sale.

Traditional lenders require a home to meet minimum property standards before they approve a loan. When a home fails to meet them, the buyer’s loan is denied, and the deal falls apart — regardless of how motivated the buyer is or how strong their credit is.

Lenders also require the buyer to carry homeowner’s insurance, and many insurance companies will not write a policy on a home with a damaged roof, outdated electrical, active plumbing leaks, unresolved structural issues, or code violations. If the home cannot be insured, it cannot be financed.

The most common issues that block financing and insurance include:

- a roof with active leaks

- foundation issues or settling that affect the structural integrity

- outdated or unsafe electrical systems, like knob-and-tube, and recalled electrical panels

- plumbing issues or failures, like corroded galvanized pipes and damaged sewer lines

- no working heater

- missing flooring

- broken windows

- fire or water damage, or mold issues

- code violations

If your home has one or more of these issues and you cannot fix them, your buyer pool is limited to cash buyers and real estate investors who do not rely on lender or insurance approval, whether you list with an agent or not. You can still list with a real estate agent, but the buyers who can actually close are cash buyers, which means you are paying 5%-6% in agent commissions to find someone who does what a direct cash buyer does without the commission.

Before you commit to any path, get cash offers first. Contact at least three cash buyers, compare what they will pay for the property in its current condition, and use those numbers as your baseline. If the cash offers are close to what you would net after agent commissions and months of carrying costs on the open market, selling directly saves you time and money.

If your home’s core systems are intact and the issues are cosmetic — outdated finishes, worn carpet, a kitchen that needs updating — your buyer pool is broader, and you have more options.

We have sold two properties to Quick Home Offers this year…

We have sold two properties to Quick Home Offers this year, dealing mostly with Adam Justiniano. Adam is very professional and made the entire process smooth both times.

Can’t afford to fix it before selling? You don’t have to.

We’ll Call You Within 1 Business Day

Enter your number. We’ll walk through your options — whether you sell to us or not. No fees. No obligation. Serving California since 2013.

Low-Cost Improvements That Actually Help — and What Improvements to Skip

If your home’s core systems are in working order — the roof holds, the foundation is stable, the electrical and plumbing work — targeted low-cost improvements can make a real difference in how potential buyers perceive the property. Not every improvement is worth the money, though.

Deep cleaning, including cleaning windows and removing excess furniture, makes spaces feel larger and more inviting. Affordable fixes like minor repairs—such as tightening loose handles, patching small holes, or fixing leaky faucets—can often be completed in under an hour and significantly improve buyer perception. When it comes to flooring, normal wear and minor scratches on hardwood floors are generally acceptable and do not require costly refinishing unless there is significant damage. These affordable fixes work because they help traditional buyers see the home as move-in ready — or close to it. When a home shows well, buyers are more likely to make competitive offers and less likely to negotiate steep repair credits after the inspection. Investing in minor cosmetic repairs, such as fresh paint and landscaping, can significantly enhance buyer perception and lead to a quicker sale at a higher price, as these improvements create a more appealing first impression.

When to Skip Cosmetic Work Entirely

Cosmetic improvements only make sense when the buyer walking through your door is someone who plans to live in the home. When the property needs a new roof, updated plumbing, a full kitchen and bathroom renovation, or major structural work, a fresh coat of paint does not raise the home’s perceived value — it raises suspicion. Buyers and inspectors start asking what the seller is trying to hide behind fresh paint on old walls.

If your buyer pool is realistically limited to cash buyers, real estate investors, and house flippers, cosmetic work is almost always wasted money. These buyers are purchasing the property for its bones and its after-repair potential, not its current appearance.

They are going to tear out the flooring, gut the kitchen, and redo the bathrooms regardless of what you do before the sale. We see this constantly — sellers paint the place and install new carpet, expecting a higher offer, but the buyer was going to demo everything anyway. That money would have been better off staying in the seller’s pocket.

If you’re in a situation where you’re behind on payments or facing foreclosure, it’s best to sell as-is because time is your most valuable resource here. Skipping putting work into the property before selling is your best route to minimize penalties and fees.

Before spending anything on improvements, ask yourself two questions: Is the buyer for this home someone who will live in it, or someone who will renovate it? And will the money I spend actually come back to me at closing? If the answer to either question is no, skip the cosmetic work and sell the home in its current condition.

Your Options When You Can’t Afford Repairs Before Selling

When your home needs major repairs, and you do not have the money to fix it, you are choosing between four paths. Each one trades off speed, effort, and how much you walk away with at closing.

Sell As Is to a Cash Buyer Directly

Sell the property in its current condition to a cash home buyer or real estate investor. No repairs, no agent commissions, no inspections, no lender approval. Closings typically happen in 7 to 21 days. This is the most common choice for homeowners whose properties need extensive repairs that would make the home unfinanceable through traditional lenders. It is also the fastest path with the least financial pressure, but you will usually net less than fixing the place up yourself and listing on the open market. Just make sure you vet the buyer when dealing directly with one. This might include obtaining a proof of funds (POF) or a letter of credit (LOC) from a construction lender. Always call the construction lender to verify the information. Ask about previous projects and referrals from other sellers.

List As Is on the Open Market With an Agent

Price the fixer upper based on comparable sales in the area, adjusted downward to reflect its condition and the estimated cost of repairs. It’s crucial to price your home accurately by factoring in repair needs and current market trends. Obtain repair estimates from contractors before setting your asking price. Buyers and their agents will get their own estimates, and if your price does not reflect the actual scope of work, you will lose credibility and offers. When selling a fixer upper in poor condition, it’s advisable to price the home low to attract investors and flippers.

This path exposes the property to a broader buyer pool, including traditional buyers, investment buyers, and house flippers interested in fixer uppers. The tradeoff is a longer timeline (typically 30 to 90+ days), 5% to 6% in agent commissions, and the risk that deals fall through after the inspection period when buyers request repair credits you cannot afford. Essentially, you’re paying an agent to find a cash buyer like Quick Home Offers® when there are many who buy direct, putting money back into your pocket.

When taking this route, consider getting a pre-listing inspection to provide transparent disclosures upfront and build trust with potential buyers. Some agents also recommend avoiding the formal “as-is” label in the listing description, as it can signal desperation and invite lowball offers.

Offer Seller Credits or Repair Concessions

List or FSBO the property and negotiate a repair credit at closing that the buyer uses to handle the work after the sale. The credit comes out of your sale proceeds, so you don’t need cash on hand. This works best when the home’s issues are manageable, and the buyer has the appetite to coordinate the repairs. It does not work well when the repairs are extensive or when the property cannot qualify for financing.

Finance the Repairs Before Selling

If you have enough equity in your home and the repairs are manageable relative to the expected increase in sales price, financing the work before listing can make financial sense. The key question is whether the money you spend on repairs will come back to you — and then some — at closing.

A home equity line of credit (HELOC) lets you borrow against your home’s equity at variable interest rates lower than those of credit cards or personal loans. Most lenders require 15% to 20% equity and a credit score in the mid-600s or higher. You draw only what you need and pay interest only on what you borrow. The downside: your home is the collateral, and expect two to six weeks from application to funding, which may not work on a tight timeline.

A cash-out refinance replaces your existing mortgage with a larger one and gives you the difference in cash. This can make sense if current interest rates are favorable, but if your current rate is significantly lower than today’s rates, you are giving up that rate on the full loan balance just to access repair funds. Run the numbers carefully.

A personal loan or home improvement loan from a bank or credit union is unsecured, so approval is faster — often within days — but interest rates are higher, typically 7% to 15% or more. Repayment periods are usually under 10 years. Personal loans work best when repair costs are in the $5,000 to $25,000 range. Retailers like Home Depot and Lowe’s also offer project financing for smaller jobs like flooring or a water heater, but read the terms closely — promotional rates often jump to 25% or higher if the balance is not paid before the promo period ends.

Some brokerages also offer concierge programs that fund repairs upfront and deduct the cost from your sale proceeds at closing – this is rare, but asking doesn’t hurt. On the buyer side, FHA 203(k) loans allow a buyer to finance both the purchase price and repair costs into a single mortgage, which can expand your buyer pool if the home needs work but is still structurally sound.

Financing repairs only makes sense when two things are true: the cost of the work is modest relative to the increase in sales price, and you have the time to complete it before you need to close. If the home needs $80,000 in work and the market will only reward $40,000 of that in a higher sale, financing is a losing proposition.

Government Grants and Low-Interest Loans for Home Repairs in California

If your household income falls below your county’s area median income limits, you may qualify for repair assistance that requires no repayment or carries rates far below what a bank would offer. The USDA Section 504 Home Repair Program provides loans up to $40,000 at a 1% fixed rate for very-low-income homeowners in eligible rural areas of California, and grants up to $10,000 for homeowners age 62 and older to address health and safety hazards. Loans and grants can be combined for up to $50,000. You can check whether your address qualifies on the USDA eligibility map.

At the state level, California’s CalHome Program funds local agencies to provide rehabilitation loans and grants to low- and very-low-income homeowners. CalHome does not lend directly to individuals — your city or county housing department administers the funds, so amounts and terms vary by location. Some municipalities offer forgivable loans that require zero repayment if you stay in the home for a set number of years, while others provide grants from $5,000 to $60,000 for critical repairs like roofing, plumbing, electrical, and HVAC. To find programs in your area, call 2-1-1 or contact your city’s housing department directly.

One thing to know: these programs are designed to help homeowners stay in their homes, not to prepare a property for sale. Some come with occupancy requirements that conflict with selling — for example, a forgivable loan that converts to a balance due if you sell within five to ten years. If the repairs your home needs exceed what these programs cover, or the application timeline does not match your need to sell, a direct cash sale may still be the more practical path.

We have sold two properties to Quick Home Offers this year…

We have sold two properties to Quick Home Offers this year, dealing mostly with Adam Justiniano. Adam is very professional and made the entire process smooth both times.

Can’t afford to fix it before selling? You don’t have to.

We’ll Call You Within 1 Business Day

Enter your number. We’ll walk through your options — whether you sell to us or not. No fees. No obligation. Serving California since 2013.

What to Know Before Accepting an Offer

If your home has issues that make it unfinanceable or you simply cannot afford the repairs, selling to a cash buyer is the most direct path to closing. The basics of how cash sales work and how to vet a legitimate cash buyer are covered in our full as-is selling guide. What most sellers in this situation don’t do — and should — is shop the deal.

Get Multiple Cash Offers Before You Decide

Contact at least three cash buyers before accepting any offer. Ask each one how they arrived at their number, what repairs they are estimating, and whether there are any fees or deductions at closing. A legitimate buyer will be transparent about their math. If someone gives you a number without explaining how they got there, move on.

The right comparison is net to net, not offer price to offer price. A $500,000 cash offer with no commissions, no repairs, and a 14-day close may put more money in your pocket than a $580,000 listing that takes four months, costs 6% in commissions, and ends with $15,000 in buyer-requested concessions after the inspection.

Ask About Creative Deal Structure To Put More In Your Pocket

Most sellers assume a cash sale means one price, one closing, done. But there are deal structures that can increase what you walk away with if you have some flexibility.

Seller financing means you act as the lender — the buyer makes a down payment and pays you monthly installments at an agreed interest rate instead of getting a bank loan. This can net you significantly more than a straight cash sale because you earn interest on top of the sale price, and it opens your buyer pool to investors and buyers who may not qualify for traditional financing. The tradeoff is that you do not get all your money at once, and you carry the risk that the buyer stops paying. Seller financing works best when you own the property free and clear or have a small remaining mortgage balance, and when you do not need the full proceeds immediately.

A profit-sharing arrangement is another option. In some cases, a cash buyer will fund all repairs and renovations and offer the seller a share of the upside when the property resells — for example, a split on anything above an agreed sale price. This is uncommon. Most investors will not consider it, and it only works on properties where the after-repair value is high enough to justify the risk for both sides. We have structured deals this way under the right circumstances, but it is the exception. It is still worth asking — the worst they can say is no.

Not every buyer will entertain creative terms, but you will never know unless you ask. Get your straight cash offers first as a baseline, then ask your top candidates whether seller financing or a profit-sharing structure is on the table.

Protect Yourself No Matter How You Sell

Always close through an independent third-party escrow and title company — never directly with the buyer. If the deal involves seller financing or creative terms, have a real estate attorney review the contract before you sign and request a credit report from the buyer. A one-time legal review typically costs a few hundred dollars and is worth every dollar on a six-figure transaction.

Frequently Asked Questions About Selling a Home That Needs Repairs In California

Can I sell my house if it needs major repairs?

Yes. You can sell a home in any condition in California. If the home cannot qualify for traditional financing due to roof damage, foundation issues, electrical problems, or other major defects, your buyer pool will be limited to cash buyers and real estate investors. If the home’s issues are cosmetic, you can list it on the open market with a real estate agent and price it to reflect its current condition. Either way, you are legally required to disclose all known material defects to the buyer.

What should I not fix before selling my house?

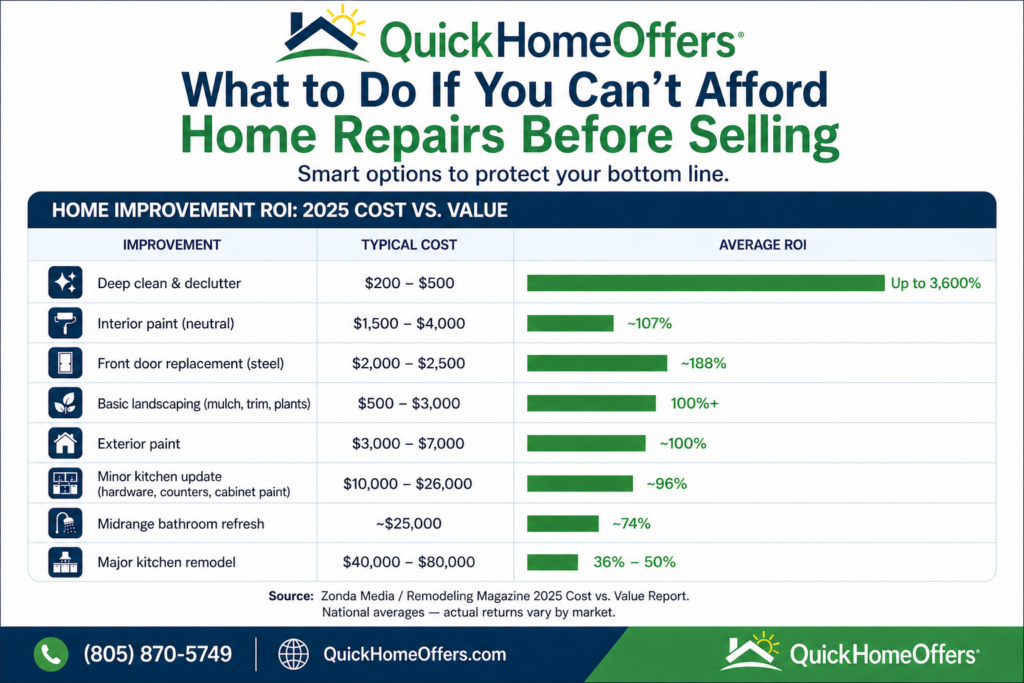

Prioritize the improvements that return the most relative to what they cost. A deep clean, decluttering, a fresh coat of neutral interior paint, and basic curb appeal like a clean front door and fresh mulch are the cheapest projects and consistently deliver the highest returns — interior paint alone averages around 107% ROI. From there, minor kitchen updates like new hardware and painted cabinets can return up to 96%, and a midrange bathroom refresh around 74%. Full kitchen remodels, room additions, and major renovations fall to 36% to 50% ROI and rarely make sense before a sale.

| Improvement | Typical Cost | Estimated ROI |

|---|---|---|

| Deep clean and declutter | $200–$500 (professional cleaning) | Very high |

| Interior paint (neutral colors) | $1,500–$4,000 | ~107% |

| Exterior paint | $3,000–$7,000 | ~100%+ |

| Front door replacement (steel) | $2,000–$2,500 | ~188% |

| Basic landscaping (mulch, trim, seasonal plants) | $500–$3,000 | 100%+ (5–15% increase in perceived value) |

| Power wash driveway and siding | $200–$500 | High (minimal cost, significant visual impact) |

| Clean or replace windows | $100–$300 (cleaning) / $3,000–$10,000 (replacement) | Cleaning: high / Replacement: ~67% |

| Minor kitchen update (hardware, countertops, paint cabinets) | $10,000–$26,000 | ~96% |

| Midrange bathroom refresh (fixtures, tile, vanity) | ~$25,000 | ~74% |

| Major kitchen remodel | $40,000–$80,000 | 36–50% |

Remodeling ROI figures are national averages from the Zonda Media / Remodeling Magazine 2025 Cost vs. Value Report. Cleaning, landscaping, and power-washing returns are general estimates and vary widely by market, condition, and scope.

If your home needs extensive work and your realistic buyer pool is cash buyers or investors, skip cosmetic upgrades entirely — they are purchasing the property for its potential, not its current appearance, and will redo the work regardless.

Can I borrow money to fix my house before selling?

Yes. A home equity line of credit is the most common option if you have at least 15% to 20% equity and a credit score in the mid-600s or higher. Personal loans and home improvement loans from banks or credit unions are available without using your home as collateral, though interest rates are higher. Low-income homeowners may qualify for government programs like the USDA Section 504 Home Repair Program, which offers loans at 1% interest and grants up to $10,000 for homeowners 62 and older. Before borrowing, make sure the cost of repairs is modest enough relative to the expected increase in sales price to justify the investment.

What repairs make a house unfinanceable?

The most common issues that prevent a buyer from getting a mortgage include a roof with active leaks, foundation problems that affect structural integrity, outdated or unsafe electrical systems, major plumbing failures, a non-functional HVAC system, missing flooring, broken windows, and unresolved fire, water, or mold damage. Another issue that comes up is code violations – active code violations generally must be addressed before conventional lenders will fund.

Lenders also require the buyer to carry homeowner’s insurance, and many insurers will not write a policy on a home with these issues. If the home cannot be insured, it cannot be financed.

Should I sell my house if I can’t afford to fix it?

If your home has health and safety issues — active mold, faulty electrical wiring, gas leaks, sewage problems, or structural damage that makes the home unsafe to occupy — selling sooner rather than later is the right move if you cannot address them. Living in a home with these conditions puts you and your family at risk, and the problems typically get worse and more expensive the longer they go unresolved. A cash buyer can close quickly and take on the remediation after closing.

If the issues are cosmetic and the home is safe to live in, you have more time to evaluate your options. Get cash offers first so you have a baseline, then compare what you might net on the open market after commissions, carrying costs, and buyer concessions.

If you want to stay in your home but cannot afford critical repairs, government programs like the USDA Section 504 program and local CalHome-funded rehabilitation programs may be able to help with health and safety repairs at little or no cost. Call 2-1-1 to find what is available in your area.

What is the 30% rule in remodeling?

The 30% rule is a general guideline suggesting you should not spend more than 30% of your home’s current market value on renovations. If your home is worth $400,000, that means capping total renovation spending at $120,000. The idea is that spending beyond this threshold puts you at risk of over-improving the property relative to comparable homes in your neighborhood, which means you will not recover the full investment at sale.

For sellers who cannot afford repairs in the first place, this rule reinforces the point: if the repairs needed approach or exceed that threshold, selling as is is likely the better financial decision.

What devalues a house the most?

The issues that reduce a home’s value the most are structural and systemic: foundation damage, roof failure, outdated electrical and plumbing systems, water damage, and mold contamination. These are the same issues that make a home unfinanceable. Beyond physical condition, deferred maintenance — peeling paint, overgrown landscaping, dirty or cluttered interiors — hurts perceived value and leads to lower offers even when the home is structurally sound. Market conditions and location also play a role, but those are outside your control. The items you can control are condition and presentation.

How do I sell an inherited house that needs repairs in California?

Inherited homes in California often come with decades of deferred maintenance, outdated systems, and personal belongings that need to be cleared out. If the property is in probate, court approval may be required before the sale can close. If the home needs major repairs you cannot afford, selling as is to a cash buyer who has experience with inherited properties is typically the fastest path. A cash buyer can purchase the home in its current condition, handle the cleanout and repairs after closing, and work within the probate timeline if needed.

About the Authors and Quick Home Offers®

Adam and Josh Justiniano are the founders of Quick Home Offers®, a California statewide cash home buying company. Since 2013, they have closed over 300 transactions across the state, purchasing single-family homes, multifamily properties, condos, and land in every condition — from homes needing minor cosmetic work to properties with major structural damage, mold contamination, and title complications.

Adam handles seller relations and personally evaluates every property before an offer is made. Josh manages marketing, underwriting, and project management for the company’s acquisitions and renovations. Every offer from Quick Home Offers is based on a hands-on evaluation by Adam or Josh — not an algorithm, not an automated valuation model, and not a junior employee reading a script.

If you are considering selling your California property and cannot afford the repairs it needs, we are happy to walk you through your options and provide a no-obligation cash offer. There is no pressure, no fees, and no commitment required.

We have sold two properties to Quick Home Offers this year…

We have sold two properties to Quick Home Offers this year, dealing mostly with Adam Justiniano. Adam is very professional and made the entire process smooth both times.

Call or text us anytime at (805) 870-5749

Or simply enter your number below, and Adam Justiniano will call you back within one business day. We will walk through your options — whether you sell to us or not.

We’ll Call You Within 1 Business Day

Enter your number. We’ll walk through your options — whether you sell to us or not. No fees. No obligation. Serving California since 2013.