How Do You Sell a House in Foreclosure in California?

Quick Answer: There are three ways to sell a house in foreclosure in California, and each fits a different situation:

- Equity sale: when your home is worth more than you owe. You pay off the lender through escrow and keep what is left.

- Short sale: when you owe more than the home is worth. The lender approves a sale for less than the balance.

- Cash sale to an investor: when the foreclosure auction is too close for a buyer to get financing. A cash buyer can close in days.

Which path fits depends on how much equity you have and how much time is left before the trustee sale. Once the auction closes and ownership transfers to the new owner, selling your home is no longer possible.

Foreclosures are becoming more common again in California. Statewide foreclosure completions rose 15% in the first quarter of 2026 compared with a year earlier, according to Attom data reported by firsttuesday, so more homeowners are facing foreclosure than they have in years. You are not the only one working through it, and you have more options than most people expect.

This guide covers California’s foreclosure timeline, your selling options at each stage, and which path protects the most equity, drawn from our experience closing 300+ properties across California since 2013, from Los Angeles to the Central Coast. If you need to sell a house in foreclosure in California and want to know how the process actually works, start here.

Want to know what your house would sell for before your sale date arrives?

Enter your number and we’ll walk through your options, whether you sell to us or not. No fees, no obligation. Trusted and experienced California cash buyers since 2013.

What This Guide Covers

Get a Cash Offer Now →- How the California Foreclosure Process Works

- California Foreclosure Timeline

- Can You Sell During Each Stage of Foreclosure?

- Your Foreclosure Selling Options Compared

- What Each Option Costs You

- How to Avoid Foreclosure Without Selling

- How California Law Protects You During Foreclosure

- Assembly Bill 2424 Explained

- Property Tax vs. Mortgage Foreclosure

- What Happens After Foreclosure

- Frequently Asked Questions

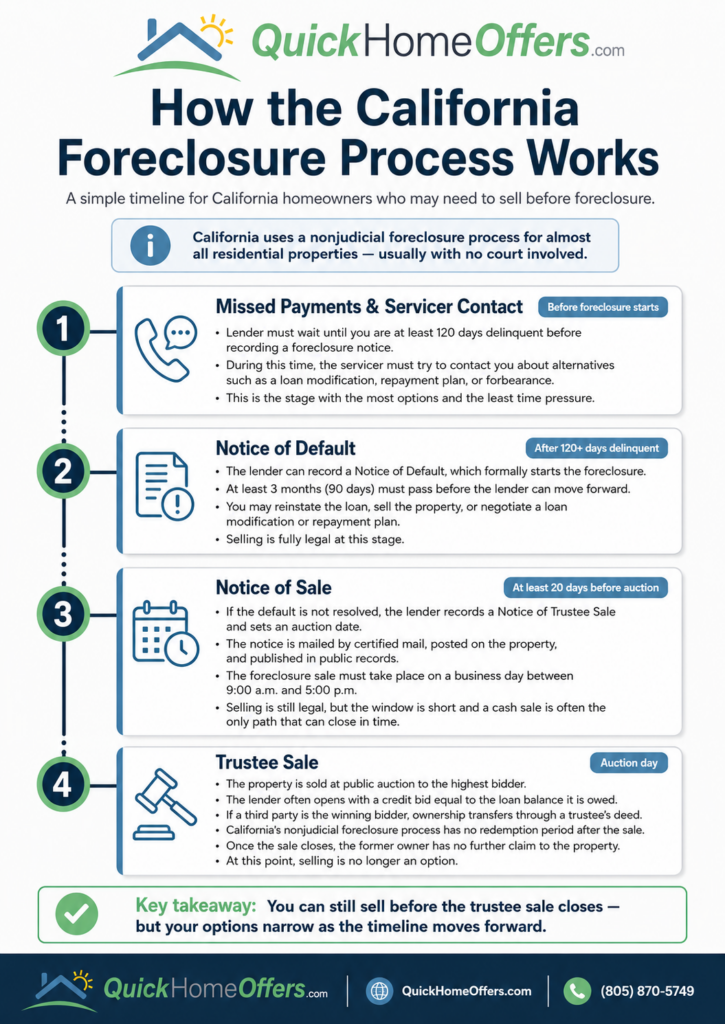

How the California Foreclosure Process Works

California uses a nonjudicial foreclosure process for almost all residential properties, which means no court is involved. Instead, your lender follows a fixed sequence of recorded notices, each with its own timing requirement under California law. The foreclosure process moves faster than most homeowners expect, and knowing where you are in it tells you exactly how much time you have left to act.

Missed Payments and Servicer Contact

Before any foreclosure notice can be recorded, federal rules require your mortgage company to wait until you are at least 120 days delinquent on your mortgage payments. During that window, the servicer must try to reach you by phone or in person to discuss alternatives such as a loan modification, repayment plan, or forbearance based on your financial hardship. This is the stage with the most options and the least time pressure, even though it rarely feels that way.

Notice of Default and the 90-Day Window

Once you pass 120 days delinquent, the lender can record a Notice of Default with the county recorder, which formally starts the foreclosure. From that recording, at least three months must pass before the lender can move forward. During this period you can reinstate the mortgage loan by paying the past-due balance plus fees, sell the property, or negotiate a loan modification or repayment plan. Selling is fully legal at this stage, and you have more time here than at any point that follows.

Notice of Sale and the Auction Date

If the mortgage default is not resolved, the lender records a Notice of Trustee Sale and sets a public auction date. In California that sale date must be at least 20 days after the notice is recorded. The trustee mails the notice to you by certified mail, posts it on the property, and publishes it in public records, and the foreclosure sale must take place on a business day between 9:00 a.m. and 5:00 p.m. Selling is still legal at this stage, but the window is short enough that a cash sale is often the only path that can close in time.

The Trustee Sale

At the trustee sale, the property goes to the highest bidder at a public auction, and the lender usually opens with a credit bid equal to the entire loan balance it is owed. Bidders typically pay by cashier’s check. If a third party becomes the successful bidder, ownership transfers through a trustee’s deed. California’s nonjudicial foreclosure process has no redemption period after the foreclosure auction, so once it closes, the former owner has no further claim to the property. This is the point at which selling is no longer an option.

California Foreclosure Timeline

The table below maps each stage of the California foreclosure process to what happens and roughly when it happens, so you can find where you are today and see how much time you likely have left to act. The notice periods come from California’s nonjudicial foreclosure statute, California Civil Code §2924 and the sections that follow it, along with the federal rule that requires your servicer to wait until you are more than 120 days delinquent before recording a Notice of Default. The typical timing column reflects those legal minimums together with what we have seen across 300+ purchases statewide since 2013. Your own timeline can run faster or slower depending on your lender, but the sequence and the minimum waiting periods are set by California law.

| Stage | What Happens | Typical Timing |

|---|---|---|

| First missed payment | Grace period, late fees assessed | Day 1 |

| 120 days delinquent | Lender becomes eligible to record a Notice of Default | ~4 months in |

| Notice of Default recorded | 90-day waiting period begins | Day 120+ |

| Waiting period expires | Lender becomes eligible to record a Notice of Sale | Day 210+ |

| Notice of Trustee Sale recorded | Auction date set, minimum 20 days out | Day 210-230+ |

| Trustee sale (auction) | Property sold to the highest bidder | Day 231+ |

| Typical full timeline | First missed payment to auction | 7-9 months |

Can You Sell During Each Stage of Foreclosure in California?

You can sell at every stage of the California foreclosure process right up until the trustee sale closes. What changes from stage to stage is not whether you can sell, but how many buyer types are still realistic and how much time you have to close. The earlier you act, the more options stay open to you.

Before a Notice of Default

At this stage, you have the most options and the most time. Nothing has been recorded against the property yet, so you can list with a real estate agent, sell privately, or sell to a cash buyer, and traditional buyers using mortgage financing can still close without foreclosure complications. This is the least stressful point to sell your home and the one that protects the most equity.

After a Notice of Default

Selling is still fully legal after a Notice of Default is recorded. The notice becomes public record, so some financed buyers may hesitate, but cash buyers and experienced real estate investors purchase at this stage regularly. You typically have about three months before the lender can record a Notice of Sale, which is enough time for most sale types to close if you start now.

After a Notice of Sale

You can still sell, but the timeline is tight. Once a Notice of Trustee Sale is recorded, you usually have 20 days or more before the foreclosure auction, and that is rarely enough time for a buyer relying on mortgage financing to close. A cash sale to an investor, or a short sale with lender approvals already in motion, are the most realistic paths at this point. You can also submit a valid listing agreement to the trustee to trigger a postponement under Assembly Bill 2424, which the law section below explains in full.

After the Trustee Sale

Once the trustee sale closes and a trustee’s deed is recorded, you can no longer sell. Ownership has transferred to the auction buyer, and California’s nonjudicial foreclosure process includes no redemption period that would let a former owner reclaim or sell the property. If you are still before the auction, this is the deadline every other decision on this page is racing against.

Your Foreclosure Selling Options in California Compared

If you decide to sell during foreclosure, you have three realistic paths to selling, plus a deed in lieu as a last resort. The right one depends on two things: how much equity you have, and how much time is left before the auction. An equity sale keeps the most money when you have significant equity and time. A short sale fits when you owe more than the home is worth. A cash sale fits when the auction is close. A deed in lieu is a last resort when none of the others can close in time. The table below breaks down the cost, timeline, and credit impact of each.

Equity Sale

An equity sale is the best outcome when your home is worth more than you owe. You sell the property, pay off the lender in full through escrow, and keep whatever proceeds remain. This stops the foreclosure completely, causes the least credit damage of any option, and leaves you with cash in hand. If you have significant equity and any meaningful time before the auction, this is the path to aim for, and listing with a real estate agent is usually how you reach the open market.

Short Sale

A short sale is for when you owe more than the home is worth. With your lender’s approval, you sell for less than the mortgage balance, and the lender accepts the reduced payoff. On most purchase-money home loans, California law prevents the lender from pursuing you for the shortfall afterward. The catch is time: short sales need lender approval that can take months, and the foreclosure clock keeps running while you wait unless you have separate protections in place. Start one only if the auction is still well out.

Cash Sale to an Investor

A cash sale is the fastest path and often the only one that works when the auction is close. There is no financing contingency, no appraisal, and no repairs, so a cash buyer can close in days instead of months. The offer reflects the home in its current as-is condition rather than what it would fetch fully repaired on the open market, which is the trade for speed and certainty when you do not have months to spend on a traditional sale. Quick Home Offers® buys at every stage of foreclosure, including pre-foreclosure homes in as-is condition, and can close before the auction date when you reach out early enough. You can see exactly how we buy houses before you decide anything.

Deed in Lieu of Foreclosure

A deed in lieu is a last resort: you voluntarily transfer the home to your lender to avoid foreclosure entirely. It can reduce credit damage compared to a completed trustee sale, and some lenders offer relocation assistance to help you move. But you walk away with no proceeds, so it only makes sense when you have no equity and no buyer who can close in time. If there is any equity in the home, one of the sale options above will almost always leave you better off.

What Each Selling Option Costs You

The table below breaks down the cost, timeline, and credit impact of each option above so you can compare them side by side.

| Option | Timeline | Out-of-Pocket Cost | Lender Approval? | Credit Impact | Keep Proceeds? |

|---|---|---|---|---|---|

| Reinstate the loan | Until 5 business days before sale | Past-due amount + fees | No | None if cured | You keep the home |

| Loan modification | 30-90 days for approval | Application costs, if any | Yes | Minimal if approved | You keep the home |

| List with agent (equity sale) | 60-120 days | 5-6% commission + repairs | No | Minimal | Yes, net after payoff |

| Short sale | 90-180+ days | Minimal (lender absorbs loss) | Yes, can take months | Moderate | No, debt forgiven |

| Cash sale to investor | 7-21 days | None (buyer pays closing costs) | No | Minimal | Yes, net after payoff |

| Deed in lieu | 30-90 days | None | Yes | Moderate | No |

| Let it go to auction | Automatic (per timeline) | None | N/A | Severe, 7+ years | Only if surplus exists |

| File bankruptcy | Immediate stay | Attorney fees ($1,500-3,500) | No | Severe | Temporary delay only |

Not sure how much time you have left before the trustee sale?

Call Adam Justiniano at (805) 870-5749. He’ll look at your situation and tell you straight what your options are, even if selling isn’t one of them. No fees, no pressure, just a real conversation about where you stand.

How to Avoid Foreclosure in California Without Selling

Selling is one way out of foreclosure, but it is not the only one. If your goal is to keep the home, several options can help you avoid foreclosure or stop foreclosure before the auction. Which one fits depends on whether your hardship is temporary or permanent, how far along the foreclosure process is, and how much you can realistically pay. The earlier you act, the more of these stay available, and your servicer is required to discuss your options to avoid foreclosure with you before it records a Notice of Default.

- Reinstate the loan. Pay the full past-due amount plus fees and you cancel the foreclosure outright. In California you can reinstate up to five business days before the trustee sale, even after a Notice of Sale is recorded.

- Loan modification. Your servicer permanently changes the terms of your mortgage, lowering the payment or extending the term so you can stay current going forward. This works best when your hardship is ongoing rather than temporary.

- Repayment plan. You keep making your regular mortgage payments and add a portion of the past-due balance on top until you are caught up. Best when a short, temporary setback put you behind.

- Forbearance. Your mortgage company pauses or reduces payments for a set period while you recover from a job loss, illness, or other financial hardship, then you resume and repay what was missed.

- Refinance. If you still have significant equity and your credit allows, refinancing into a new loan can replace the defaulted one. This gets much harder once a Notice of Default is recorded, so it works best early.

- Bankruptcy. Filing triggers an automatic stay that halts the foreclosure sale immediately, but it is a temporary stop, not a cure, and it carries serious long-term consequences. Treat it as a last resort and talk to a bankruptcy attorney first.

Homeowners facing foreclosure rarely have just one path, and the right foreclosure defense is whichever one you can actually execute in the time you have left. If none of these are realistic and the numbers do not work, selling before the auction is the option that protects your remaining equity, and the earlier sections of this guide cover how to do that at each stage.

How California Law Protects You During Foreclosure

California’s Homeowner Bill of Rights gives you specific, enforceable protections during foreclosure, and most homeowners never learn they exist until it is too late to use them. The three below matter most when you are trying to keep your home or buy time to sell.

Dual Tracking Is Prohibited

Your servicer cannot push the foreclosure forward while it is reviewing a complete loan modification application. If you submit a complete first-lien loan modification application at least five business days before a scheduled sale, the servicer cannot record a Notice of Default, record a Notice of Sale, or hold the trustee sale while that application is pending, until it issues a written decision and any appeal period has passed. If your servicer forecloses in violation of this rule, you can sue to stop the foreclosure, and if the sale has already happened, you may be able to recover damages.

You Can Reinstate Up to 5 Business Days Before the Sale

You have the right to stop foreclosure by paying the full past-due amount plus fees and costs, and that right runs until five business days before the trustee sale. It does not end when the Notice of Sale is recorded. If you can pull together the arrears, even late in the process, reinstatement cancels the sale and you keep the home.

Your Servicer Must Reach Out Before Recording a Notice of Default

Before your lender can record a Notice of Default, it must try to contact you at least 30 days earlier, often through letters and phone calls, to review your financial situation and walk through options to avoid foreclosure. During that contact it has to tell you that you can request a meeting, which must be scheduled within 14 days. If the servicer skips this step, it can be grounds to challenge the foreclosure.

Watch Out for Foreclosure Rescue Scams

Homeowners facing foreclosure are targets for fraudulent companies that promise to stop foreclosure for an upfront fee, ask you to sign over your deed, or tell you to send mortgage payments to them instead of your lender. Legitimate help is free. You can talk to your lender at any time, and the U.S. Department of Housing and Urban Development maintains a free list of HUD-approved housing counselors. Before you work with anyone, learn how to spot foreclosure rescue scams so a bad actor does not cost you the home you were trying to save.

These protections can buy you time, but none of them erase what you owe. If keeping the home is not realistic, selling before the auction is what protects your equity, and the options earlier in this guide cover how to do it at each stage.

Looking To Sell To a Reputable California Cash Buyer?

A word on who you’re talking to. We are not a foreclosure rescue service, and we never charge a fee to make you an offer. We are California cash buyers who have purchased homes in pre-foreclosure since 2013.

If anyone asks you to pay upfront to stop your foreclosure, that is the warning sign to walk away. Talking to us costs nothing and puts a real number in front of you to compare against everything else on the table.

Assembly Bill 2424: The Law Most Sellers Don’t Know About

Assembly Bill 2424 can give California homeowners in foreclosure up to 90 extra days to sell, and almost no one facing a sale date knows it exists. Effective January 1, 2025, AB 2424 lets you postpone the trustee sale twice, simply by showing the trustee you are actively working to sell the property.

The first postponement comes from a listing agreement. If you deliver the trustee a valid listing agreement with a California-licensed real estate broker at least five business days before the scheduled sale, the trustee must postpone the auction by at least 45 days. The listing has to be a genuine effort to sell the home, placed on a public marketing platform, and it must be sent by certified mail or a tracked overnight courier so there is confirmed proof of delivery. A late or undocumented submission does not count.

The second postponement comes from a purchase agreement. If you find a buyer during that window and deliver the trustee a signed purchase agreement at least five business days before the rescheduled sale, the trustee must postpone again by at least another 45 days. Together that is up to 90 days past your original auction date to close a sale. Each postponement can be used only once, and the purchase price generally has to be enough to pay off what you owe.

AB 2424 also added a price floor at the auction itself. The lender must give the trustee a recent fair market value of the property at least 10 days before the first sale date, and the trustee cannot accept a winning bid below 67% of that value at the initial foreclosure sale. This protects more of your equity even if the property does go to auction.

One honest detail: the first postponement requires a licensed broker listing, so a cash sale by itself does not start the AB 2424 clock. But once a listing is in place, a signed purchase agreement, including a cash offer, triggers the second 45-day extension, and the full window is time any sale can close in. If your auction is close, the move is to get the listing step handled and a buyer who can actually close inside that window.

Property Tax Foreclosure vs. Mortgage Foreclosure: They Are Not the Same

Most foreclosure advice assumes you are behind on your mortgage. If you are behind on property taxes instead, you are in a completely different process with a very different timeline. Mortgage foreclosure runs through the Civil Code and a bank, and it can reach a trustee sale in as little as 7 to 9 months. Property tax foreclosure runs through the Revenue and Taxation Code and your county tax collector, and for a residential home the county generally cannot sell it until the property has been tax-defaulted for at least five years.

That five-year runway is the biggest practical difference. Under California Revenue and Taxation Code §3691, a residential property reaches “power to sell” status only after five or more years of tax-default, compared with three years for nonresidential commercial property. Throughout that period, and right up until the last business day before the public auction, you can redeem the property by paying the full defaulted taxes plus penalties, which accrue at 18% per year, along with a redemption fee. You have far more time than a mortgage foreclosure allows, but the balance keeps growing the entire time. If a lien is the issue, our guide to tax liens in California explains how property tax, FTB, and IRS liens get paid through escrow.

The reason this distinction matters: the moves that work for a mortgage foreclosure do not apply to a tax sale. There is no loan to reinstate, no short sale to negotiate, and no AB 2424 listing postponement, because there is no mortgage lender involved. The clock, the paperwork, and the resolution options are all different. If you are not certain which process you are in, check who sent the recorded notice. A lender and trustee means mortgage foreclosure. The county tax collector means property tax foreclosure.

Either way, you can still sell before the auction. Quick Home Offers® buys properties with delinquent property taxes the same way we buy any other home, and in most cases we handle the tax payoff through escrow at closing, so the back taxes come out of the sale proceeds instead of out of your pocket up front.

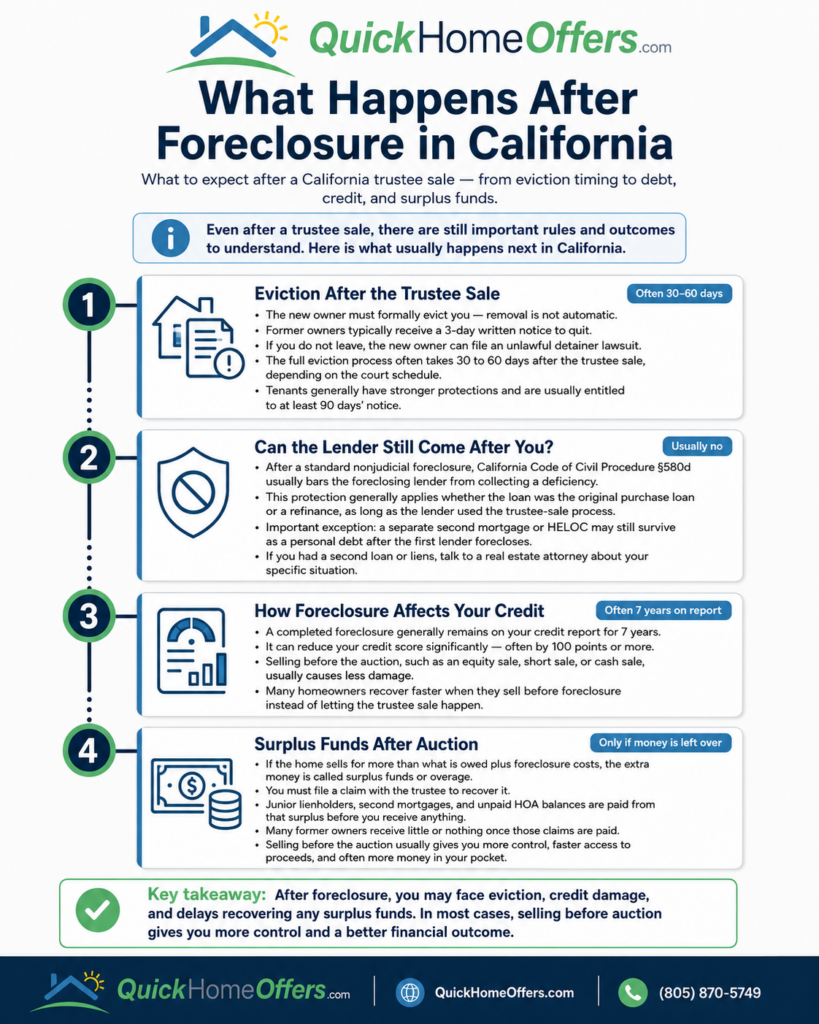

What Happens After Foreclosure in California

If the trustee sale does happen, a few things follow, and knowing them ahead of time helps you plan even at the last stage. Here is what to expect after a California foreclosure, from eviction timing to whether you still owe anything.

Eviction After the Trustee Sale

Once the property sells, the new owner has to formally evict you. You are not removed automatically. As the former owner, you typically receive a three-day written notice to quit. If you do not leave, the new owner files an unlawful detainer lawsuit, and the full eviction process usually takes 30 to 60 days from the trustee sale, depending on the court’s schedule. Tenants living in the property have stronger protections and are generally entitled to at least 90 days’ notice.

Can the Lender Still Come After You for the Balance?

Usually no. After a standard nonjudicial foreclosure, California Code of Civil Procedure §580d bars the foreclosing lender from pursuing you for a deficiency, the gap between what you owed and what the property sold for. This protection applies whether your loan was the original purchase loan or a later refinance, as long as the lender used the trustee-sale process, which is what nearly all California foreclosures use. You can read a plain-English explanation of California’s anti-deficiency laws from a licensed California real estate firm.

The exception that surprises people is a second loan. If you had a separate second mortgage or HELOC and your first lender forecloses, that junior lender’s security is wiped out by the sale, and they may still be able to sue you on that separate debt. This is the one situation where you could owe money after foreclosure. If you also need to sell a house with liens in California or you have a second loan on the property, talk to a real estate attorney about your specific situation before you assume you are clear.

How Foreclosure Affects Your Credit

A completed foreclosure generally stays on your credit report for seven years and can lower your score substantially, often by 100 points or more. A sale before the auction, whether an equity sale, short sale, or cash sale, typically causes less damage and lets you recover faster. Many homeowners who sell before foreclosure qualify for conventional financing again within a few years, while a completed foreclosure on the credit report makes that harder for longer.

Surplus Funds After Auction (and Why You Usually Get Less)

If your home sells at auction for more than you owe plus foreclosure costs, the extra money, called surplus funds or overage, belongs to you. But getting it is neither fast nor guaranteed. You have to file a claim with the trustee, and junior lienholders, second mortgages, and unpaid HOA balances are paid out of that surplus before you see a dollar. Many sellers who count on an overage end up with little or nothing once those claims clear.

Compare that to selling before the auction. In an equity sale or a cash sale, you control the timing, you pay off the loan through escrow, and you keep what is left with no trustee claim process and no junior liens jumping ahead of you. In most cases a pre-auction sale puts more money in your pocket than waiting on an auction surplus, and it puts it there sooner.

Frequently Asked Questions About Selling While in Foreclosure in California

Can you sell your house before it goes to auction in California?

Yes. California law lets you sell at any point before the trustee sale takes place, during the Notice of Default period, during the Notice of Sale period, and right up until the foreclosure auction begins. The closer you are to the sale date, the fewer buyer options you have, so a cash sale is often the only path that can close in the final weeks.

How many missed payments before foreclosure starts in California?

Federal rules require your servicer to wait until you are more than 120 days delinquent before recording a Notice of Default, the first formal step. In practice, most lenders begin after three to four missed payments. That 120-day window is meant to give you time to apply for a loan modification, repayment plan, or another option to avoid foreclosure.

How do you stop a foreclosure sale in California?

You have several ways to stop a foreclosure sale: reinstate the loan by paying the past-due balance up to five business days before the sale, get a loan modification or repayment plan approved, sell the property before the auction, or file bankruptcy for an automatic stay. Submitting a listing agreement under AB 2424 can also postpone the sale by 45 days. Which option fits depends on how much time and equity you have.

What is the new foreclosure law in California?

The newest major foreclosure law is Assembly Bill 2424, effective January 1, 2025. It lets a homeowner postpone the trustee sale by at least 45 days by giving the trustee a valid listing agreement with a licensed California broker, and by another 45 days with a signed purchase agreement, for up to 90 extra days to sell. It also sets a minimum auction bid of 67% of the property’s fair market value at the first sale.

How many times can you postpone a foreclosure in California?

Under AB 2424 you can postpone the trustee sale up to two times based on your own efforts to sell, once with a listing agreement and once with a purchase agreement, for up to 90 days total. Separately, the foreclosure trustee can postpone a sale at its own discretion up to three times before it has to publish a new notice of sale. Your lender may also postpone for its own reasons, such as a pending loan modification review.

What is the 37-day foreclosure rule?

The 37-day rule is a federal protection. If you submit a complete loss-mitigation application, such as a loan modification request, more than 37 days before your scheduled foreclosure sale, your servicer must evaluate you for all available options and generally cannot hold the sale while it does. If you submit it 37 days or fewer before the sale, the servicer is not required to follow those rules, so applying early matters.

Do I need a lawyer to stop foreclosure in California?

No, a lawyer is not required to stop foreclosure. You can reinstate the loan, apply for a loan modification, or sell the property without one. An attorney can help if your situation involves a lender violating your rights or a dispute over a second loan, but many homeowners avoid foreclosure by selling or curing the default on their own.

Can you sell a house with a reverse mortgage in foreclosure?

Yes. A reverse mortgage can enter foreclosure when the borrower passes away, moves out, or falls behind on property taxes or insurance, and the heirs or borrower often need to sell quickly. Because a reverse mortgage balance grows over time, there may be little equity left, so the timeline matters even more than with a traditional mortgage. You can sell the home to pay off the reverse mortgage before the foreclosure auction, and a cash sale is often the fastest way to do it.

Do I still owe money after a foreclosure in California?

Usually not on the foreclosed loan. After a standard nonjudicial foreclosure, California law bars the foreclosing lender from pursuing you for the shortfall, whether the loan was your original purchase loan or a refinance. The exception is a separate second mortgage or HELOC. If your first lender forecloses, that junior lender can sometimes still sue you on that separate debt, so check with a real estate attorney if you had more than one loan.

Is it better to let a house foreclose or sell it?

Selling is almost always better than letting the home go to a foreclosure auction. A sale before the auction, whether an equity sale, short sale, or cash sale, protects more of your equity, causes less credit damage, and lets you recover faster. A completed foreclosure stays on your credit report for seven years and usually leaves you with less than a pre-auction sale would, especially after junior liens and fees reduce any auction surplus.

Do I get money if my house sells at a foreclosure auction in California?

Sometimes. If your home sells at auction for more than you owe plus foreclosure costs, the surplus, also called overage funds, legally belongs to you. To claim it you file a claim with the trustee, but junior lienholders, second mortgages, and unpaid HOA balances are paid out of that surplus first, so many former owners receive little or nothing once those claims clear. Selling before the auction usually puts more money in your pocket and gets it to you faster.

What is the fastest way to sell a house in foreclosure in California?

A cash sale to a direct buyer is the fastest way. There is no financing contingency, no appraisal, and no repairs, so a cash purchase can close in as little as 7 to 21 days, often the only timeline that works when the auction is close. Quick Home Offers® buys houses, multifamily, condos, and land at every stage of foreclosure, even condemned or red-tagged homes, and can close before your auction date when you reach out early enough.

Does Quick Home Offers buy houses in foreclosure?

Yes. Quick Home Offers® buys houses, multifamily properties, condos, and land at every stage of foreclosure, from the first missed payment through an active Notice of Sale. We pay cash, cover all closing costs, and can close before your auction date when contacted early enough, including properties with delinquent property taxes or in pre-foreclosure as-is condition.

Can I get cash before closing?

On qualifying properties, Quick Home Offers® can provide a cash advance before closing for sellers who need to relocate or cover immediate expenses. The advance is deducted from your final sale proceeds at closing through escrow. Ask us about your situation when you reach out.

This article is for informational purposes only and is not legal advice. If you need legal advice about your foreclosure, consult a licensed California attorney.

We’ll Call You Within 1 Business Day

Enter your number. We’ll walk through your options — whether you sell to us or not. No fees. No obligation. Serving California since 2013.

If your sale date is coming and you want to know what a cash sale would actually net you, we’ll give you a straight answer. Adam or Josh looks at your property personally, not an algorithm, and makes you a no-obligation cash offer you can weigh against your other options. Call (805) 870-5749 or submit your address below. The earlier you reach out, the more room you have to work with.

About the Authors and Quick Home Offers®

Adam Justiniano is co-owner of Quick Home Offers® and works directly with sellers across California. He visits properties, meets with homeowners, and walks them through their options. Adam has been buying real estate since 2013 and has handled foreclosure and pre-foreclosure situations involving Notices of Default, tight trustee-sale timelines, reverse mortgages, liens, and homes in serious disrepair. When a sale has to close before an auction date, he is the one on the phone with the seller. He grew up in Ventura County and still lives there today.

Josh Justiniano is co-owner of Quick Home Offers® and runs the company’s underwriting, financial analysis, and project management. He evaluates the numbers behind every offer the company makes, including the net proceeds a seller would walk away with after a loan payoff, lien resolution, and closing costs. Josh worked at a legal firm in Thousand Oaks before entering real estate at 21, which gave him an eye for the documentation and title work that time-sensitive foreclosure transactions require. He attended California State University of Northridge and majored in real estate. He and Adam have closed over 300 property transactions across California since 2013.

Quick Home Offers® is a California cash home buying company headquartered in Thousand Oaks, CA. The company purchases houses, condos, multifamily properties, and land statewide, including homes in foreclosure and pre-foreclosure. Every offer is personally evaluated by Adam or Josh, not generated by an algorithm. To speak with them directly, call (805) 870-5749.